In this post I’ll show how to start making your own forecasts and financial models for a company you’re thinking about investing in.

Finding Coca-Cola using combinatory screening filters

First let’s find a company that’s interesting enough, by using a free online screener. There are many good screening tools to choose from, such as investing.com, KoyFin, Wallmine, Finviz etc.

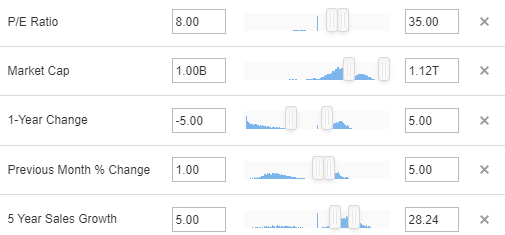

I like to combine a few valuation filters with a few stock price filters, an industry filter (e.g., Consumer Non-Cyclicals) as well as some fundamental filters like revenue growth or profitability. For this exercise let’s go with the following filter settings at investing.com, including the mentioned industry filter:

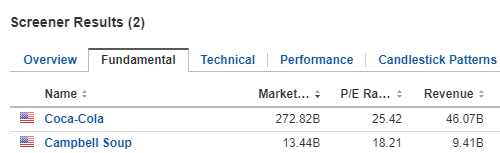

I got 2 hits in the US from that search:

Let’s go with Coca-Cola. We could have chosen just any company, and please note that these filter settings were mainly chosen at random and are not fine-tuned for finding the best possible investment out there. You will have to choose your own settings, based on the type of investment that suits your investment style and asset portfolio.

We can see that the stock was basically flat over the last year as requested (+/- 5% filter), and up by 17% over three years. Add another 10%-points to account for Coca-Cola’s dividends to get to the 3-year total return of about 27%.

Now let’s switch to KoyFin do do some research on Coca-Cola’s historical growth and profitability patterns, as well as its typical valuation ranges, in order to make forecasts for A) profit per share, B) P/E-ratio, C) stock price => annualized total returns. And then assess whether that return is good enough to warrant an investment

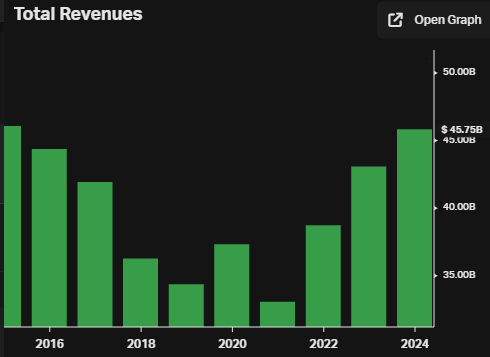

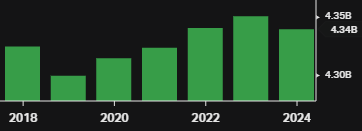

We start by looking at KO’s accounting highlights for the past 10 years

In the free version of KoyFin you can access a chart of 10-year data by hovering over the green diagram symbols to the left of each variable you’re interested in. The most important numbers are Total Revenues (=sales), Net Income Margin, and EPS (Earnings Per Share, i.e., profits)

Sales numbers are flat over the last ten years, marked by declines the years 2014-2020, and strong growth of about 17% in one single year (2021), however barely making up for the decline the previous year.

All in all, KO’s sales were slightly lower in 2023 than in 2014. A pretty bad record!

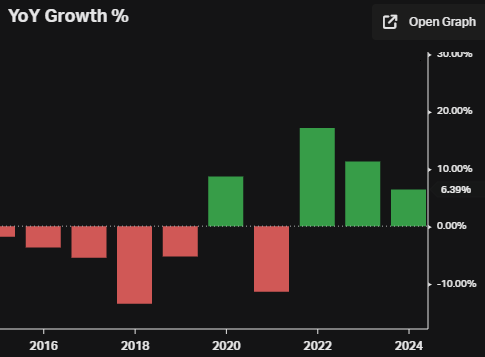

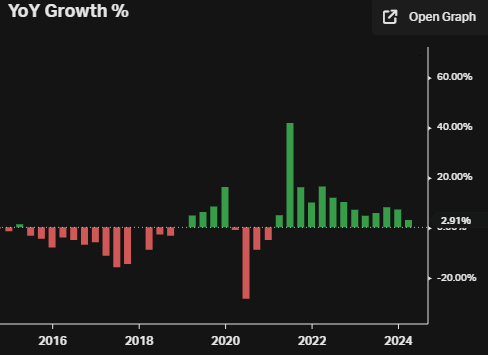

Switching to quarterly data, the impact of the pandemic lockdowns and the subsequent recovery is even more visible.

The Q1 2024 growth rate was just 3%, despite having a pretty easy first quarter last year (5%) as the starting point.

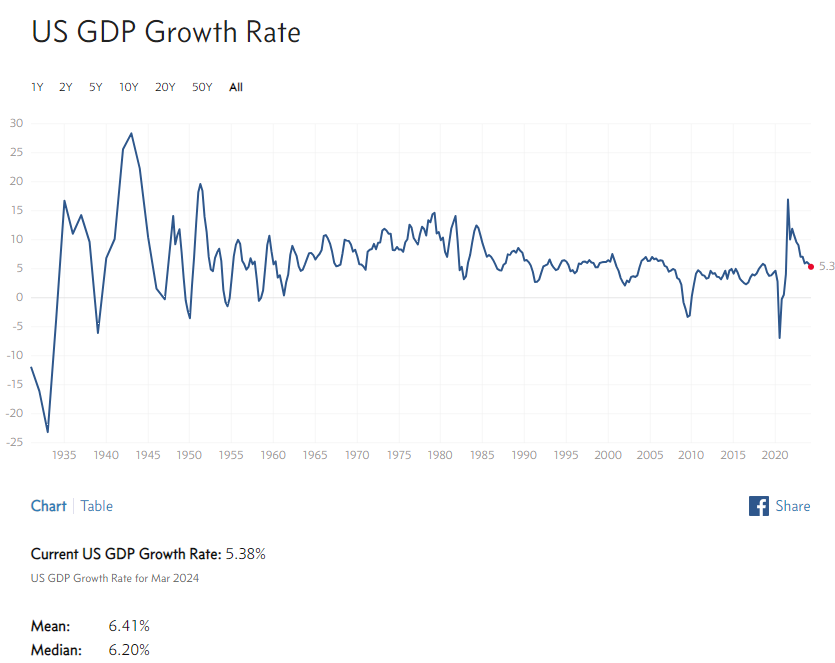

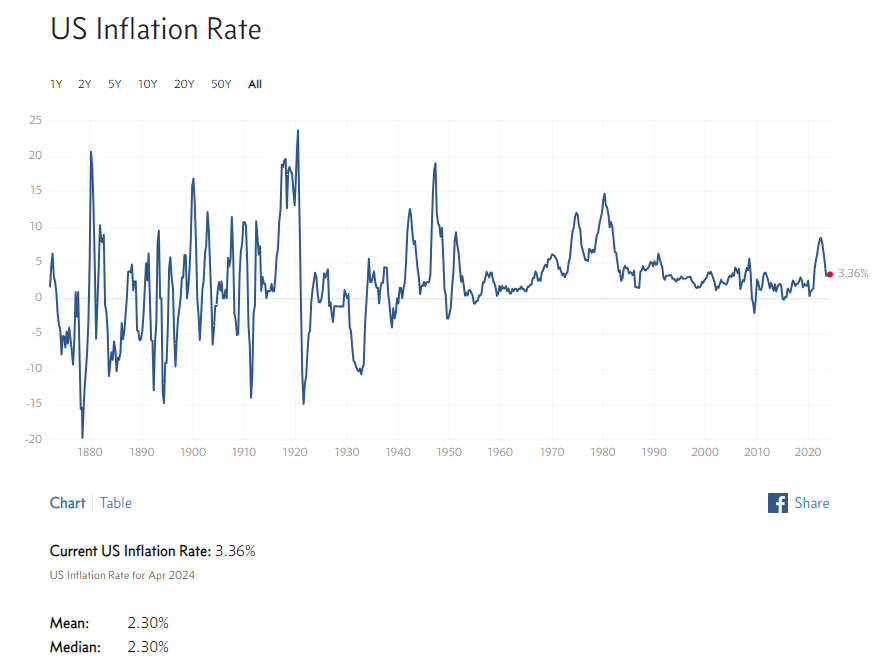

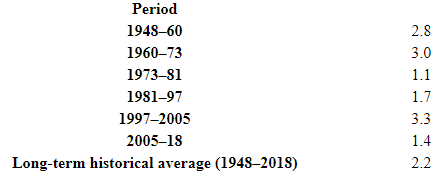

Given these growth patterns I would hesitate to forecast any faster growth for KO than low to mid single digit percentages. But let’s be generous and say that KO can manage to grow sales by the long average for the general US economy: 5-6% nominal growth per year (Note: not the “real”, inflation-adjusted growth rate that is commonly cited), consisting of about 2% in employment, 2% productivity and 2% price increases (the actual long term average for price increases in the US is 2.3%, population growth has been 1.0%, and productivity growth 2.2% per year).

The most recent GDP (nominal) growth number was 5.3%, which actually is closer to the most recent half-century average than the previous half-century average growth rate. Growth is slowing down, due to all the easy gains already being made from industrializing the nation. Computers, the internet and smartphones aren’t enough to push growth higher.

You can check the long term averages for various macro data components at Shiller (multpl.com), or go directly to sites like FRED or macrotrends.

Productivity numbers from bls.gov (%):

Perhaps the economy and KO will get a little boost from higher price increases the coming decade and push nominal growth all the way up to 6% per year:

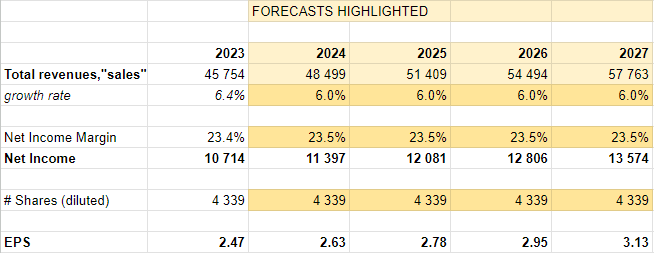

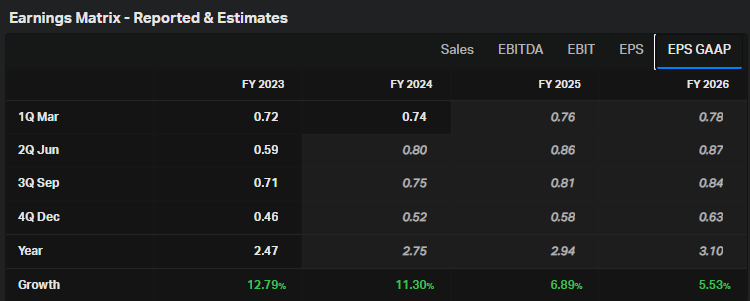

Coca-Cola financial model. Sales forecasts

Next up is KO’s profits. Let’s start with its Net Income Margin. It isn’t the most precise or recommended way to do this, but it works well enough for our example. If you want to learn these methods more in detail you should check out The Investing Course.

It looks stable enough around the most recent level of 23.5%, so let’s go for that forever. Now we have a profit forecast, and can also calculate the profit per share, EPS, assuming a stable share count going forward.

The share count has remained constant around 4.33B

Let’s see what the consensus view is at KoyFin, under Analyst Estimates/Estimates Overview/EPS. It’s pretty close to my forecast. Well KO is a really boring and predictable company, so no surprises there. But does it make for a good investment?:

Historical valuation patterns

The forward looking P/E-ratio (based on the current share price relative to the EPS forecast for the coming 12 months) for KO has typically held between 20-25, and the current value according to KoyFin is right in the middle at 22.2. My calculation differs slightly from theirs, as I get 22.7 based on my 2025 EPS forecast.

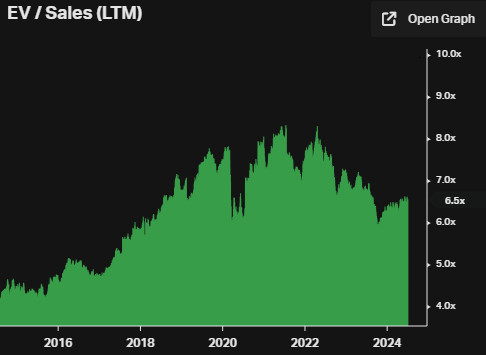

The backward looking EV/S multiple (based on actual reported sales numbers) went through a step change between 2014 and 2018, and has since then fluctuated between 6-8x. It’s currently sitting at 6.5x, slightly below the newfound average.

Is 6.5x really at the low end of the relevant range, or might the EV/S valuation be trending back down toward the pre-2018 level again? On the other hand, sales growth numbers were negative earlier and warranted a lower valuation if the trend continued.

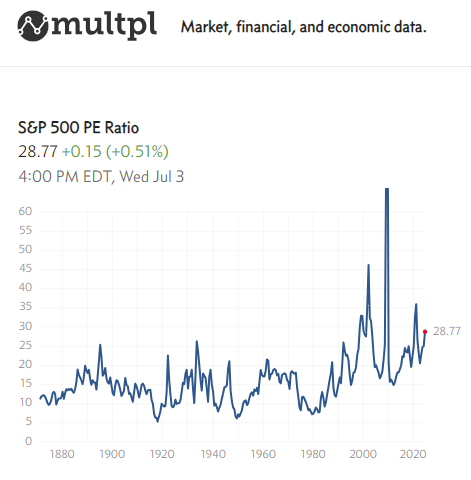

S&P 500 is currently valued at 29x earnings according to multpl.com, but its typical range has been between 10-20x for an average of about 15x. As Hussman regularly demonstrates, when buying the S&P index at 15x, the investor has historically enjoyed a subsequent 10% compound annual total return, which apparently a century of stock market wisdom has deemed fair compensation for taking diversified equity risk. That 10% CAGR is composed of 8% profit growth and 2% dividend yield. The growth rate is 2%-points better than the economy, simply because the 500 top US companies are better run than the economic average.

Note: Since 1990, the 15x P/E mark has become more of a floor than an average, without any improvements in growth characteristics. That simply means investors have settled for lower future total returns. There’s nothing inherently wrong with accepting a likely 8% per year instead of 10% total return, but bear in mind that is what is being done when paying a significantly higher multiple than the historical average.

That is by the way also the case with Coca-Cola. KO is growing in line with the economy, which is a couple of percentage points lower than for the average S&P 500 company. Hence, KO should be valued a bit lower than the average company, i.e., lower than P/E 15 if we are to rationally expect a 10% annual total return.

But let’s not get too much into details here. Perhaps 15x can be warranted after all. At least KO is stable and predictable and does distribute a decent dividend of 3% per year, rather than the typical 2%. KO is thus close enough to represent the economy in general or the average S&P 500 company.

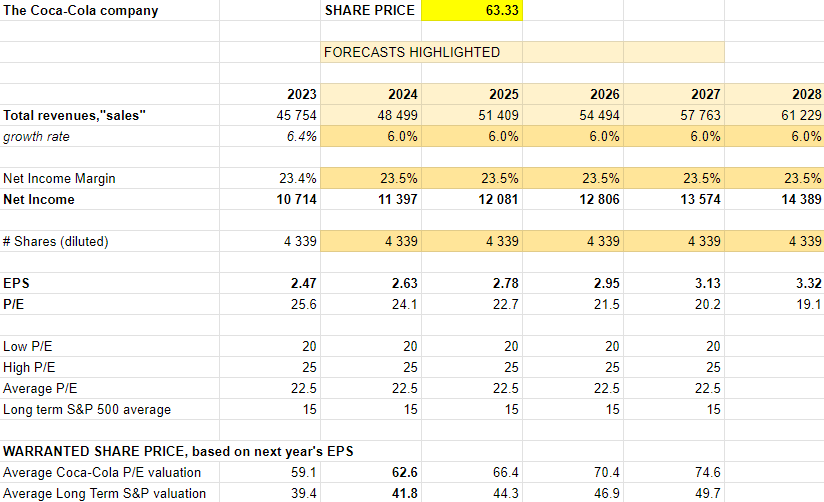

Final model and warranted share price

Updated model, with warranted share prices a given year, based on average P/E-valuations for next year’s EPS forecast

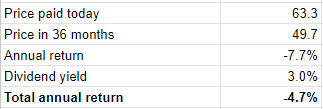

So, when we are here in 2024, we could value KO at 22.5 times the 2025 EPS of $2.78, which amounts to $62.6 per share, which is about where it’s trading today. That’s what the market has settled for in KO’s case

Alternatively we could choose to set the fair price at the L-T S&P 500 average of 15x, which would result in $42 per share today, $44 next year, $47 the year after that, and finally $50 per share in 2027. That series of 6% annual share price appreciation plus a dividend yield of 3% would give the investor a 9% total return — not great, not even good, but perhaps sufficient to feel protected against holding cash or bonds instead.

Now think about what would happen if you paid $63 today and the price dropped to its actual fair value of $50 three years from now. You would lose 5% per year.

Remember that I’ve been pretty generous in all parts of the calculation. I could just as well have chosen 5% annual growth, or 4% for that matter, instead of 6%. I mean, it’s been 0% on average for the last ten years, so even 0% isn’t out of the question.

And a net margin of 23.5% for selling sugar water and other drinks is definitely not a given right. KO has to fight for that result every day.

I also was generous with the fair valuation multiple of 15x when 13-14x would have been more reasonable considering KO’s lower growth than average. If even lower growth than that would materialize the market could sooner or later punish KO with yet lower multiples. At zero growth a 10x multiple might be warranted instead of 15x, let alone 22x.

Concluding remarks

In any case, this was never meant as a thorough analysis of Coca-Cola. I just wanted to show how you can use free online resources to quickly establish pretty robust patterns of growth, profitability and valuation multiples, which can be used to estimate future total returns from a stock purchase.

Then the real research can begin, which among other things entail understanding what Coca-Cola is actually doing, and how long they can be assumed to keep doing it.Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.