I talked to Bernstein associates for an hour earlier today. “What’s your worst trade ever?”. “What’s top of mind for you now?”

1) Short eurozone banks (listen to the audio file for details)

2) Real assets, because inflation isn’t at all dead

Real assets, case in one point: URC

I talked more about this in the upcoming audio file. For now let’s just recall that the problems of government debt and deficits aren’t over; quite the contrary, they have just begun. Consequently much more fiat currency as well as fiscal stimulus will be needed to keep kicking the can down the road.

That means crack up boom times for real assets (including stocks, but eventually they will lose momentum vs real real assets due to inflation and higher interest rates, not to mention an increasingly less effective economy (cf Argentina the last 20, 50 or 100 years)

Real assets include electrification minerals and infrastructure: rare earth elements, cobalt, nickel, copper; electricity generation, energy storage systems, frequency balancing systems, gold, silver, bitcoin, ether, real estate…

In the uranium space…

…my bet is on URC, the only uranium royalty company (comparable with Franco Nevada in the gold space). You currently basically get their entire royalty portfolio for free, since their holdings of physical uranium has a market value on the same order of size as their entire market capitalization:

Understanding the Value Proposition of URC: A Comprehensive Overview

Key Financial Insights:

Uranium Assets: URC possesses 2.6 million pounds of uranium, valued at approximately CAD 350 million, which contributes significantly to the company’s total market capitalization of CAD 400 million.

Royalties: The current royalty portfolio is essentially valued at zero, providing an attractive proposition for investors.

Projected Cash Flow from Royalties:

2027: Estimated cash flow of $10 million.

2030: Projected cash flow increases to $20 million.

2033: Annual cash flow expected to reach $50 million, equivalent to CAD 70 million.

These figures highlight the robust potential returns from the existing royalty portfolio, which investors are currently acquiring for free.

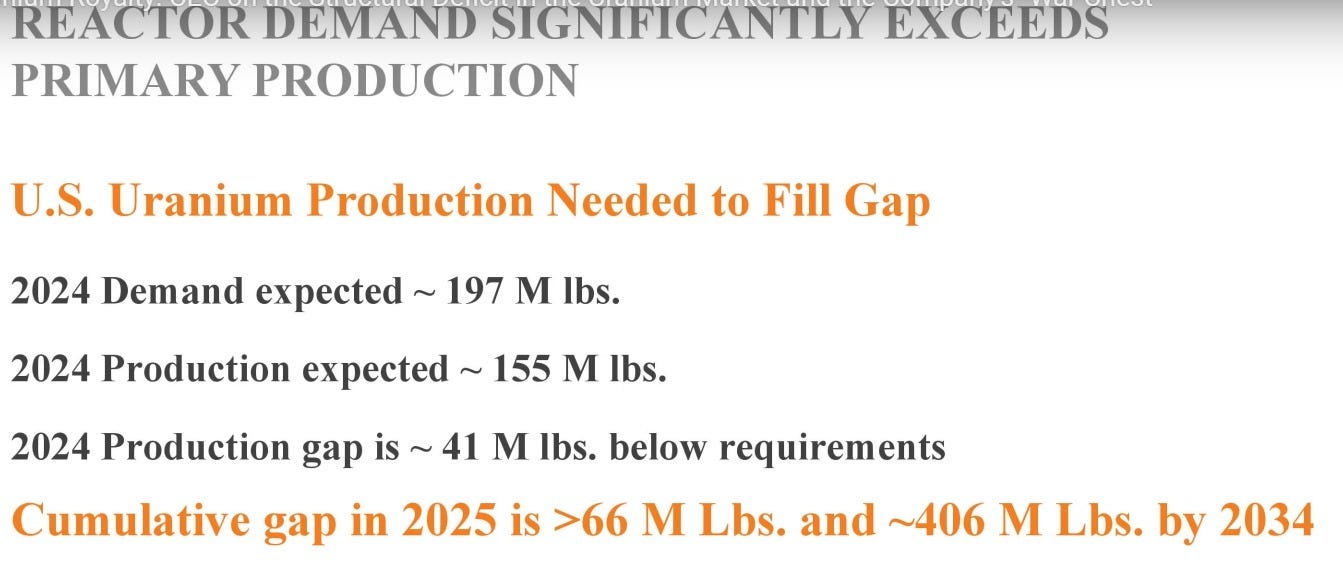

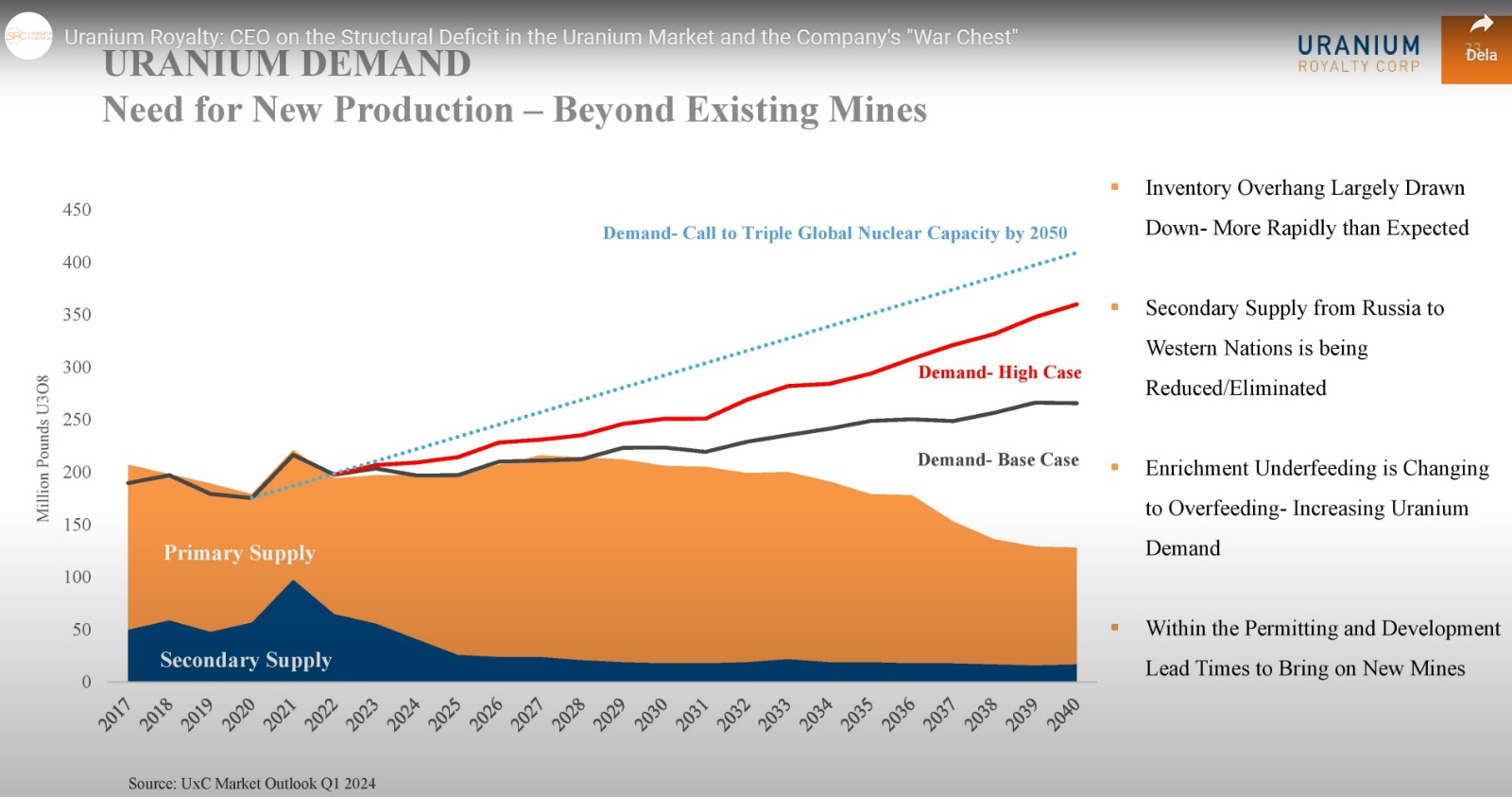

Detailing the uranium supply deficit:

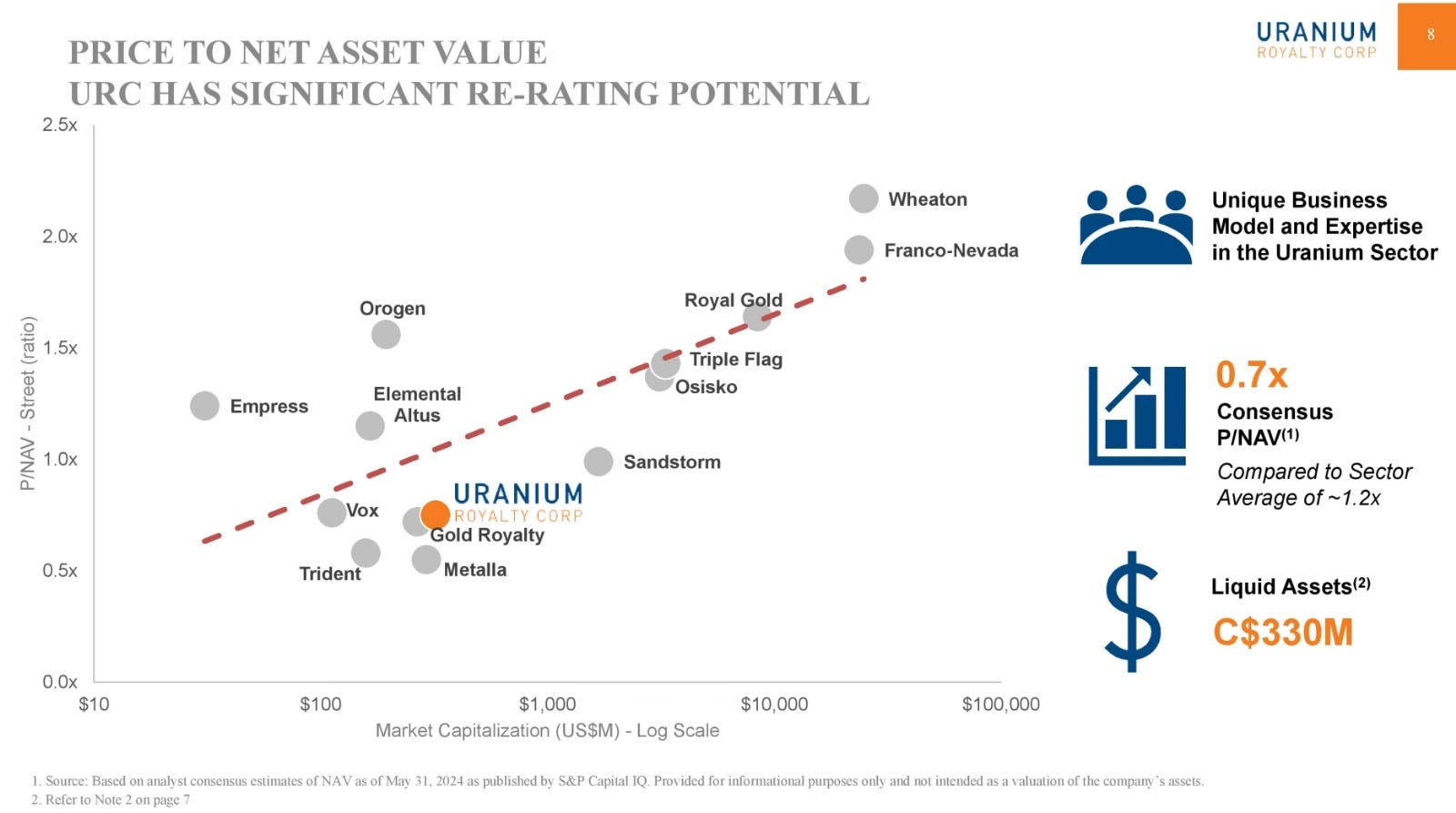

Comparative Analysis with Franco-Nevada:

Franco-Nevada Valuation: Gold royalties are valued at 18 times sales.

URC Potential Valuation: Applying this multiple to URC’s royalties in 2033 results in a valuation of CAD 1.25 billion for existing royalties. Including earnings accumulated until 2033 (approximately CAD 175 million), the total becomes around CAD 1.4 billion, to be discounted to present value or realized over a decade.

Impact of Uranium Price Increase:

Uranium Price Scenario: A potential 50% increase in uranium prices would significantly enhance URC’s valuation.

2033 Projections: In this scenario, URC could generate CAD 350 million in cash flow by 2033. With an 18x cash flow valuation multiple, this would add CAD 2.5 billion to URC’s worth. Including the uranium portfolio valued at CAD 500 million, the total valuation would reach CAD 3 billion.

Future Growth: Adding new royalties and uranium purchases could push the valuation to (at least, I’d dare say) CAD 3.2 billion, i.e., 8 times the current 400m market cap.

Investment Perspective:

Current Stock Price: URC’s stock is currently priced at CAD 3.30, presenting a substantial growth opportunity.

Long-Term Growth: The projected valuation indicates a potential 8x increase from the current market value, translating to three doublings over nine years, or an annual growth rate of approximately 25%.

Conclusion: fairly valued, i.e., a potential 10-bagger over a decade

Investing in URC offers a compelling opportunity with significant long-term upside, particularly if uranium prices rise. While the immediate term may not see a dramatic surge in stock price unless uranium prices suddenly increase sharply, the projected steady growth presents a reasonable and even attractive return on investment for exposure toward one of few solutions to increasing demand for reliable energy (as opposed to unreliable weather dependent renewables). This makes URC a “good, not great” investment with a reasonable expectation of reward for patient investors.

TIP: this is not financial advise

TIP too: keep an eye on the silver space the coming 12 months! This is my watchlist:

Addendum: update after a reader comment